Feb 3, 20265 min read

The 15-Second Window: Behavioral Fraud Detection Without Friction

95% of legitimate users don't act within 15 seconds of a deposit. That single insight changed how I think about fraud detection forever.

95% of legitimate users don't act within 15 seconds of a deposit. That single insight changed how I think about fraud detection forever.

Most fraud detection adds friction. Extra verification steps. SMS codes. "Is this really you?" pop-ups.

Every one of those steps kills conversion. Legitimate users abandon checkouts, close apps, and call support. You stopped the fraud but you also stopped the revenue.

There's a better way. I learned it building fraud systems in iGaming, and the core insight is embarrassingly simple.

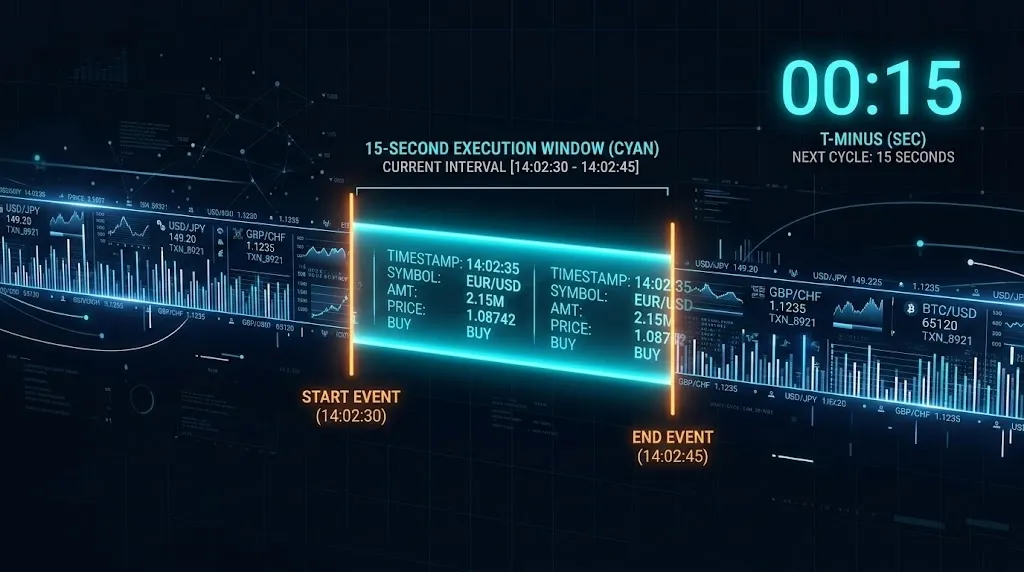

In iGaming, the flow is: user deposits money, then places a bet.

When I analyzed millions of deposit-to-first-action sequences, one pattern dominated everything else: 95% of legitimate users do not place a bet within 15 seconds of depositing. (Outliers for specific event days, daytime excluded from this post to make it easy to understand.)

They browse. They check odds. They look at their balance. They think.

Fraudsters don't think. They deposit with a stolen card and immediately move the money — a bet, a withdrawal request, a transfer. Speed is their entire strategy because they know the clock is ticking before the card owner notices.

That 15-second gap is a behavioral signal more reliable than any rule engine I've built.

Once you see this pattern, you stop thinking about fraud detection as "check every transaction" and start thinking about it as "evaluate the behavioral window."

During the deposit:

| Signal | What it tells you |

|---|---|

| Device fingerprint | New device? Known fraud device? |

| Deposit velocity | Third deposit in 10 minutes? |

| Amount pattern | Round number? Matches a known testing pattern? |

| IP geolocation vs account region | Mismatch? |

| Card BIN history | This BIN associated with previous chargebacks? |

These signals are evaluated during the deposit, not after it. The user never sees a loading screen because the evaluation happens in parallel with the payment processing.

During the 15-second window:

If the deposit signals are clean, let it through. No friction.

If the deposit signals are ambiguous — not clearly fraud, but not clearly clean — watch the post-deposit behavior:

deposit_time = now()

first_action_time = await_first_action(user, timeout=15s)

gap = first_action_time - deposit_time

if gap < 15s AND deposit_signals.score > THRESHOLD:

flag_for_review() # or block the action

elif gap < 15s AND deposit_signals.score < THRESHOLD:

allow() # signals were clean, fast action is fine

else:

allow() # normal behavior

The beauty of this: zero friction for 95% of users. They never know the system is watching. They deposit, they browse, they act. The system has already cleared them before they even make a decision.

I wrote about behavioral fraud detection years ago. Traditional detection layers rules:

The 15-second window is none of these. It's a behavioral invariant. It doesn't need training data. It doesn't need a model. It's a product design decision: use the natural pause in user behavior as a free evaluation period.

You're not adding a step. You're using a step that already exists.

The pattern generalizes. Any platform where users deposit/load funds and then act has this gap:

Fintech / Neobanks:

E-commerce with wallets:

Crypto exchanges:

The specific timing threshold changes. In iGaming it was 15 seconds. In banking it might be 30 seconds. In e-commerce it might be 2 minutes. The principle doesn't change: legitimate users have a natural decision gap that fraudsters skip.

Find your gap. Measure it. Design around it.

This approach has one hard requirement: you need to process deposits and post-deposit actions as a single behavioral session, not as independent events.

Most fraud systems evaluate transactions in isolation. "Is this deposit suspicious?" and "Is this bet suspicious?" are separate questions asked by separate systems.

To use the behavioral window, you need the deposit evaluation to persist and inform the post-deposit evaluation. That means:

This is more engineering work than a stateless rule engine. But the payoff — zero friction for legitimate users and higher catch rates for fraud — makes it one of the highest-ROI fraud investments I've made.

"What about legitimate users who act fast?"

They exist. Power users who know exactly what they want. Regulars who deposit and immediately place their usual bet.

The 15-second window is not a hard block. It's a signal amplifier. A fast action from a user with 2 years of clean history on a recognized device in their usual region is fine. The speed alone doesn't trigger anything.

A fast action from a new account, new device, new card, unusual amount? The speed amplifies every other signal. That's the combination that triggers review.

Behavioral signals are not binary. They're weights.

Fraud detection doesn't have to be a tax on your users. The best systems are invisible to legitimate customers and devastating to fraudsters. Find the behavioral gap. Use the time your users naturally give you. Stop adding friction to solve a problem that behavior already solves.